Skip to content

theSatoriReport

Celebrities

Beauty

Fashion

Lifestyle

Sport

TV & Movies

World News

Search for:

Celebrities

Zara Tindall: I was obviously very lucky that my mother didnt give us any titles

Posted on

12/21/2023

Weezer's Rivers Cuomo Teases 'Epic Tour' In Celebration Of 30th Anniversary Of 'Blue Album'

Posted on

12/21/2023

Romesh Ranganathan breaks silence on staggering weight loss

Posted on

12/21/2023

Travis Scott's Drink Explodes After He's Hit By Loose Ball During Nets Game

Posted on

12/21/2023

Beauty News

Discover the World of OPI Gel: Nail Artistry Perfected

Posted on

10/06/2023

Woman lambasted for blow-drying her own hair at the salon

Posted on

09/29/2023

Salud y Belleza

Posted on

09/25/2023

Smell like the phone book with the new Eau de Yellow Pages perfume

Posted on

09/19/2023

12 Products Comedian Hannah Berner Can't Live Without This Fall

Posted on

09/13/2023

Paco Rabanne now does makeup – we tried it and here's our verdict…

Posted on

09/11/2023

Fashion News

‘Don’t do it!’ beauty fans plead in horror as 90s trend makes an official comeback with influencers | The Sun

Posted on

12/21/2023

We stopped shopping at Aldi after too many bad experiences – now we don't waste our money and shop at Tesco and M&S | The Sun

Posted on

12/21/2023

I’m a 32DDD and tried the Skims nipple bra, you girls have no idea how amazing life is about to get, she’s a 10/10 | The Sun

Posted on

12/21/2023

The chilling ‘clues’ mummy blogger who confessed to child abuse left on YouTube for her millions of followers to see | The Sun

Posted on

12/21/2023

Lifestyle

I am in my 60s and having amazing sex – this is how I stay fit

Posted on

12/21/2023

'Absolute heaven' scream Home Bargains shoppers over 99p giant box of classic party snack that's ideal for Christmas | The Sun

Posted on

12/21/2023

Homebase shoppers rush to buy 'fantastic' 6ft inflatable Santa the 'kids love' down to £25 from £50 in Christmas deal | The Sun

Posted on

12/21/2023

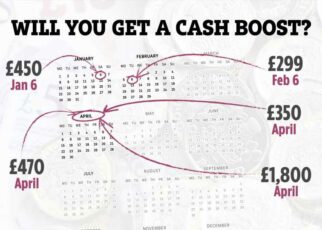

Exact dates in 2024 millions will get cash boosts worth up to £3,299 – will you be better off? | The Sun

Posted on

12/21/2023

TV & Movies

I am in my 60s and having amazing sex – this is how I stay fit

Posted on

12/21/2023

Zara Tindall: I was obviously very lucky that my mother didnt give us any titles

Posted on

12/21/2023

UK 'probably' has to accept EU migrants under Starmer returns plan

Posted on

12/21/2023

Weezer's Rivers Cuomo Teases 'Epic Tour' In Celebration Of 30th Anniversary Of 'Blue Album'

Posted on

12/21/2023

Sport News

Meet Viddal Riley who trained YouTube star KSI for his fight against Logan Paul and was signed by Floyd Mayweather | The Sun

Posted on

12/21/2023

I was a top jockey who died for seven seconds after a fall – now I'm back training winners for Harry Redknapp | The Sun

Posted on

12/21/2023

Transfer news LIVE: Chelsea beating Newcastle for wonderkid, Tottenham eye £26m defender, Phillips in Juventus talks | The Sun

Posted on

12/21/2023

Plans for new Super League unveiled after shock court ruling including 64 teams, three divisions and knockout finale | The Sun

Posted on

12/21/2023

AI simulates Anthony Joshua vs Otto Wallin with referee forced to intervene after 'barrage of body shots' | The Sun

Posted on

12/21/2023

Liverpool's Caomhin Kelleher forced to remove PIE from pitch after object appears to be thrown from West Ham end | The Sun

Posted on

12/21/2023

World News

UK 'probably' has to accept EU migrants under Starmer returns plan

Posted on

12/21/2023

Hamas ‘REJECTS offer for week-long ceasefire in exchange for 40 hostages’ despite net closing on terror boss Sinwar | The Sun

Posted on

12/21/2023

Striking French cops ‘missed chance to save Alex Batty MONTHS ago when he went to school…then made same crucial blunder’ | The Sun

Posted on

12/21/2023

British teenager Alex Batty could have been found five months earlier

Posted on

12/21/2023

Knifeman guilty of murdering girlfriend and three family members

Posted on

12/21/2023

How Brianna Ghey's murderer went from schoolgirl to fantasist 'witch'

Posted on

12/21/2023

Recent Posts

I am in my 60s and having amazing sex – this is how I stay fit

Zara Tindall: I was obviously very lucky that my mother didnt give us any titles

UK 'probably' has to accept EU migrants under Starmer returns plan

Weezer's Rivers Cuomo Teases 'Epic Tour' In Celebration Of 30th Anniversary Of 'Blue Album'

Meet Viddal Riley who trained YouTube star KSI for his fight against Logan Paul and was signed by Floyd Mayweather | The Sun